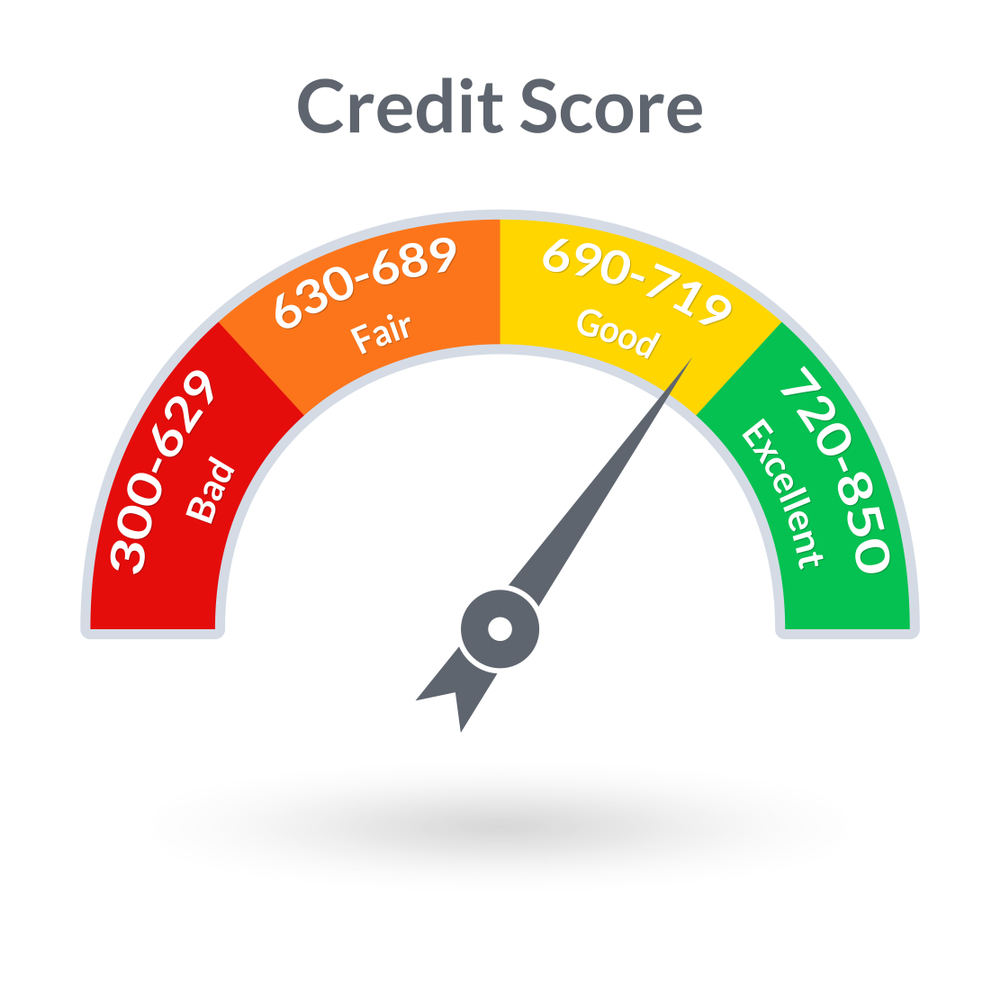

Your FICO credit score for mortgage lending is one of the first things lenders consider. It influences the types of loan programs you qualify for, your interest rate, and even the size of your down payment. In short, the higher your score, the more buying power you unlock. But don’t worry — even if you’re not at the top of the scale, options exist.

")